Table of Contents

Key Takeaways

- Continuous accounting, unlike traditional accounting, centers on speed and efficiency without sacrificing data integrity.

- Transitioning to implement continuous accounting is both cost-effective and empowering for teams.

- Creating a continuous accounting workspace involves changing the culture, not just software.

Accounting operates most effectively with accurate, real-time data. But until recently, this was either cost-prohibitive for most businesses or too challenging to implement. Rapid technological advancement has led to a shift from manual accounting to automated processes and customizable tech stacks, as well as a new form of accounting.

Continuous accounting, as opposed to traditional models, throws out time-consuming manual tasks and streamlines day-to-day activities. It reduces the stresses of short accounting periods with 24/7 access to data and removes some of the most tedious tasks, such as invoice reconciliation.

But this isn’t just a technology shift towards accounting automation. It also demands finance teams move away from siloed and lengthy reports to collaborative and short-form but granular reporting. As a result, finance and accounting teams are more important than ever for decision-makers looking to identify opportunities in an uncertain market.

What is a continuous accounting model?

A continuous accounting model is a method of accounting in which teams conduct period-end tasks on an ongoing basis. In a continuous accounting model, data is delivered continuously, providing real-time visibility into transactions and reconciliations.

A typical record-to-report period-end accounting process takes weeks to complete and comes with frustrating downsides, including delayed visibility and human error. This prevents finance teams and business leaders from performing the real-time analysis necessary to inform fast decision-making. You are either left waiting on new information or forced to rely on outdated data.

Conversely, when companies adopt a continuous accounting model, they achieve faster close periods, immediately identify errors and potential fraud, and make quick, intelligent decisions - not to mention the time saved on tedious manual reconciliation. Continuous accounting allows you to be efficient, agile, and strategic.

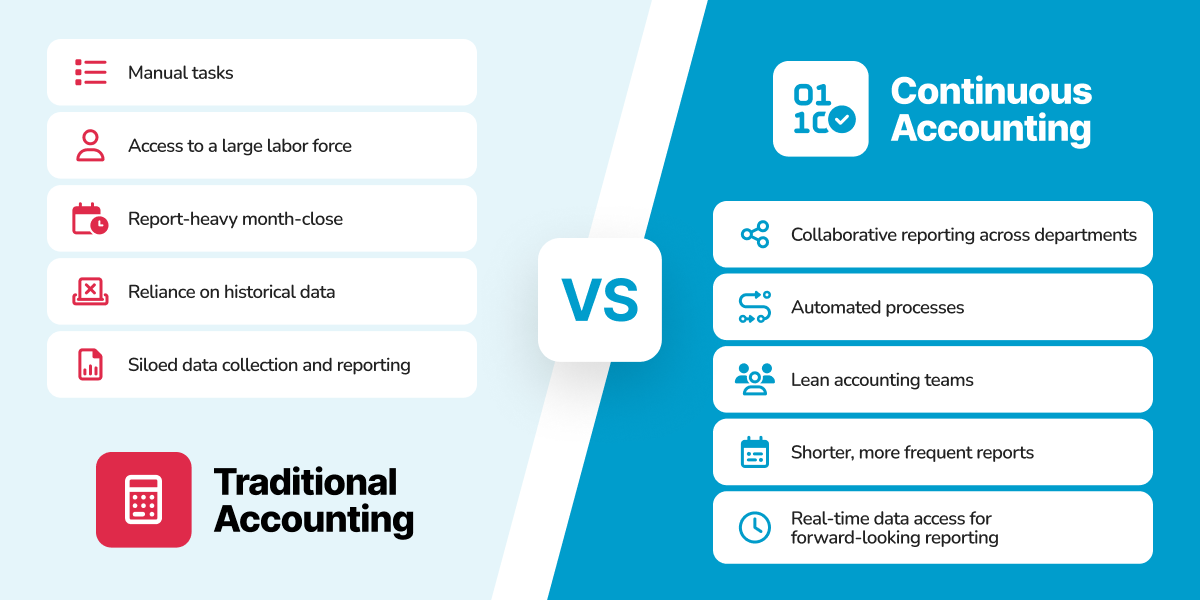

Traditional vs. Continuous Accounting

Traditional accounting stems from the pre-cloud, pre-real-time days of number crunching. Fewer and fewer firms hold to traditional accounting processes, and for good reason. This model is built on a foundation of:

- Manual tasks

- Access to a large labor force

- Report-heavy month-close

- Reliance on historical data

- Siloed data collection and reporting

In other words, the entire mode of accounting is inefficient and outdated. Meanwhile continuous accounting stresses:

- Collaborative reporting across departments

- Automated processes

- Lean accounting teams

- Shorter, more frequently reports

- Ongoing accounting work rather than workflows built around month-close

- Real-time data access for forward-looking reporting

- Full procure-to-pay visibility

The benefits of continuous accounting

Today’s finance teams must adjust quickly as they grapple with tightened budgets, a distributed workforce, and new macroeconomic risks. Many will do that by leveraging digital tools that can expedite their processes. In a PwC Pulse CFO survey, 62% of respondents reported having accelerated use of automation and digital technologies, and 75% anticipated more resources going to digital tools and services in 2021.

Many companies have embraced digital transformation, leveraging technology to unite and empower their increasingly remote workforces. Individual employees are seizing their autonomy to purchase the things they need to do their jobs, without going through the traditional centralized channels that were built for the old way of doing business.

A recent survey found that 80% of non-C-suite employees now have a say in purchasing decisions — and that was before the explosion of remote work in 2020. With more business spend originating from more places than ever before, finance teams need real-time visibility into what’s happening across the company.

Traditional accounting cycles cannot offer the kind of transparency needed to update forecasts, reprioritize investments, or reallocate capital as conditions change — they just move too slowly. Today’s business landscape demands a modern, agile strategy, which only a continuous accounting cycle can facilitate.

Continuous accounting is the new way to work

According to a recent report from EY, finance leaders will play a critical role in businesses recovery from the COVID-19 crisis. They will need to move with agility as they work to safeguard revenue, reduce costs, and lay a solid foundation for future growth.

But traditional accounting cycles, characterized by long timelines and low levels of visibility, make agile operations challenging. Modern finance requires a more seamless and real-time workflow to get the data the team needs, when they need it. Only with a continuous accounting cycle can finance teams lead a truly agile finance department.

4 foundations to a continuous accounting model

Accounting values accuracy and reliability of accounts. Continuous accounting lends itself to these principles of continuous accounting through its foundational pillars:

- Automate process. The underlying technology that makes continuous accounting possible is automation, whether that be through robotic process automation (RPA) or artificial intelligence (AI). Accounting automation tools streamline repetitive tasks to drastically reduce human error, accelerate the accounting process, and make reporting and fraud detection easier than ever.

- Analyze Consistently. Thanks to real-time data and automation, accounting professionals can regularly assess real-time financial records, investigate suspicious transactions, and identify opportunities.

- Centralized reporting. Quality continuous accounting processes and software will consolidate spend information, break down departmental siloes, and simplify the reporting process—all without compromising data integrity.

- Empower Teams. Continuous accounting requires ensuring your team has the financial data and structures to successfully and quickly wrap up accounting tasks each month.

How to create a continuous accounting model

By following the below steps, you can build a continuous accounting model to inform smarter, faster decision-making.

1. Enable remote and distributed teams to work effectively from anywhere

With nearly half of companies allowing employees to work remotely full-time, finance departments must implement systems that enable their increasingly distributed teams to comply with policy no matter where they are.

The first step in that process? Moving finance operations to the cloud. Remote teams can be more agile when they’re not bound to outdated systems and processes, such as sharing physical corporate cards and submitting paper receipts.

Moreover, cloud-based operations allow you to review and analyze corporate spend in real time, continuously. Finance teams can immediately track every purchase as it happens and, as a result, make immediate adjustments to budgets and policies.

2. Increase visibility into spend

One of the biggest challenges with a traditional accounting cycle is that finance teams may not become aware of purchases until the virtual card statements come in at the end of the month. Maintaining real-time visibility eliminates this time delay, so they can respond in real time and make smart decisions, faster.

To ensure ongoing real-time spend insights, you need systems that allow you to track purchases—both completed transactions and funds that have been committed to a vendor but not yet spent—against the budget. Distributed spend management software allows you to see this financial information—as well as payment methods, receipts, and other purchase data—all in one place.

By correctly coding transactions upfront, finance teams can get visibility into purchases before they occur. This information is seamlessly transmitted to the company’s accounting software, granting you an unprecedented level of transparency.

3. Automate and unify your processes

Finance automation saves time for the accounting team and ensures all employees get what they need more quickly. By reducing disparate and time-consuming manual processes, your team is freed to focus on more strategic work that delivers on the company’s bottom line.

Automated reconciliation saves you time on month-end close by taking on the manual grunt work. Transaction data is seamlessly passed through to your accounting software - including QuickBooks, NetSuite, Intacct, and Xero - which helps you on your way to a continuous close. This reduces manual errors and allows employees in and out of finance to view accurate data at any given time, not just at month-end closing.

Enabling a system that automatically guides employees through the correct purchasing workflow ensures compliance without relying on employees to remember your expense policy and act accordingly. With distributed spend management software, a conversational interface notifies employees of the steps they need to take, and proactive controls guarantee that all spend is within policy and budget.

What are the best software solutions for implementing a continuous accounting model in my finance department?

Theoretically, any platform that offers real-time data, automation, and centralized spend data can act as a continuous accounting software. This includes ERPs like Netsuite and Sage Intacct, accounting software like Quickbooks or Xero, or specialized integrations like Paystand or Teampay.

Integrations often provide another layer of security, automation, and efficiency to ERPs and accounting software. For example, Paystand provides notarized receipts for AR teams, and Teampay offers full spend insights and approval automation, among other features.

Which consulting firms offer services to help adopt a continuous accounting model?

Most consulting firms will offer continuous accounting models assistance. The more important questions are whether these firms will match your company goals, budget, and what particular solutions they recommend. Not all spend management software is created equal, and it is worth shopping around, even with the help of a consulting firm.

How can my business transition from traditional accounting to a continuous accounting model for improved efficiency?

The first step to transitioning from a traditional account process to a continuous accounting model is mapping your system. Then you can identify points for automation and collaboration, making it easier to evaluate potential software solutions.

Once you know what features you need, you can begin shifting from manual processes to automated rules for accounting. As you free up more time from transforming each accounting task, the transition often becomes easier and faster.

Working with a software solution that offers significant training can provide additional support and speed up the process.

What are the top benefits of investing in a continuous accounting model for corporate finance teams?

Corporate finance teams benefit from continuous accounting models through:

- Reduced costs of human errors

- Leaner teams

- Scalable process

- Enhanced fraud and opportunity deduction

- Easier to capture early payment discounts

- Improved vendor relationships

- Time saved from manual processes

Set your team up for success

With the right processes and technologies, you can achieve a truly continuous accounting cycle. This will allow your team to make smarter, faster decisions, elevating your position in your organization and driving agility in an ever-changing market. After implementing Teampay and using the continuous accounting model, Copper was able to reduce month-end close to just 3–4 days.

At Teampay, we pride ourselves on providing a comprehensive spend management platform and in-depth training for accounting teams. We empower finance professionals with feature like:

- Invoice automation

- Approval automation

- Accounts payable automation

- Purchase request conversation capture

- Spend policy automation

- Real-time data reporting

- Centralized spend data

- And more